I focused on the daylight robbery occurring the past few years of some RM40 to 50billion (TO DATE, and still RISING!...) from 1Malaysia Development Berhad, and we all know who's the One who should be held Reesposible and Accountable, don't we? That's WHY Desi says "MO1 Bukan PM Saya! MO1 is NOT my.PrimeMinister". Note my. can stand for MAlaysia, YES!

From the ever-reliable Sarawak Report cometh this update:~~~~

Today at 9:06 AM

|

"Malaysians Underestimate The Trouble Their Country Is In" - The Economist Spells It Out Over The 1MDB Issue29 November 2016

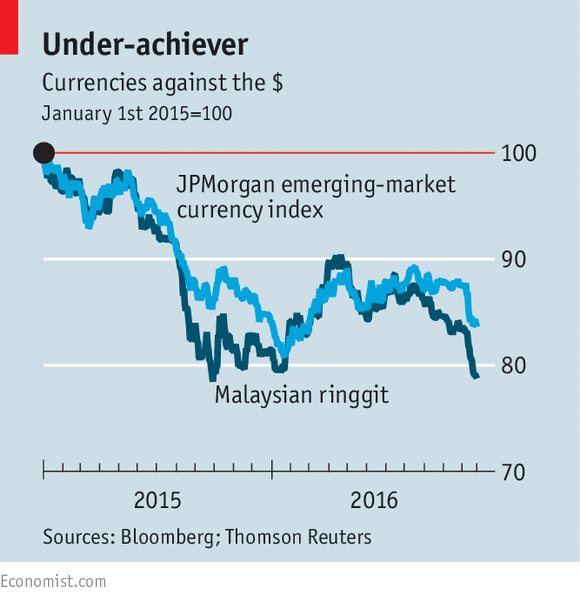

Tainted analysts with vested interests in managing Malaysia’s corruption, like the ‘Asia Wealth Management’ boss for the bank UBS, have been putting themselves about the media in recent days, trying to talk up the ringgit.

But, it isn’t working. Excuses are being made for the continuing decline of the currency, such as ‘The Trump Effect’, when everyone knows the real problem is ‘The Najib/1MDB Effect’.

For the past fortnight the true dire state of the ringgit has been disguised by Najib’s tame new Central Bank Governor, who has been wasting the country’s reserves by throwing huge sums at buying up the currency, which everyone else is sensibly getting out of.

He has made it fundamentally worse by lecturing banks that they must stop the frantic selling, thereby proving the desperate nature of the crisis.

The fact of the matter is that no one wants to invest in a country which is run by a coven of criminals, who are locking up people left, right and centre in an arbitrary fashion for complaining that the rule of law is not being upheld.

No one wants to invest in a country where all respectable people from all sides of the political divide have been forced to unite in condemnation of a thief Prime Minister, who refuses to quit office.

It is particularly telling for observers of Malaysia that this is a country where it remains possible for a man to remain in office, despite having been exposed as a kleptocrat billionaire – who on earth can consider their money safe under the jurisdiction of such a man and his bought and corrupted cohorts, who are making up the rules as they go along to slap down anyone who points out the truth?

Because the UMNO leadership control the local media, these goons are still living in a mental bubble, telling themselves that they can keep up their crackdown and eventually obedience and order will reassert itself in their favour. But, this is not Operation Lalang, not least because Mahathir was competent and everyone can see that Najib is not.

Najib may succeed in continuing to hold on to power by attacking protestors, locking up the opposition, encouraging extremism and violence and then cheating the election, but the price will be a tumbling ringgit and poverty for all. Malaysians are used to a better life and they will not thank UMNO for this.

Hard copy version

See the leader below in the UK’s respected ECONOMIST magazine – followed by its financial comment:

Malaysians underestimate the damage caused by the 1MDB scandal |

Police nab Red Shirts leader, Jamal Yunos on eve of Bersih 5 rally

Police nab Red Shirts leader, Jamal Yunos on eve of Bersih 5 rally United Nations (UN) Special Rapporteur slams pre-Bersih arrests

United Nations (UN) Special Rapporteur slams pre-Bersih arrests The Edit: Riding high dunes in a Nissan Navara

The Edit: Riding high dunes in a Nissan Navara The Edit: Corey Lee is Eater Chef of the Year

The Edit: Corey Lee is Eater Chef of the Year